Blog

Coming to Terms with Income Tax Scrutiny in India Getting notice from Income tax department for scrutiny simply gives stress to every individual/ businesses. The term “scrutiny”

Coming to Terms with Income Tax Scrutiny in India Getting notice from Income tax department for scrutiny simply gives stress to every individual/ businesses. The term “scrutiny”

The Crucial Connection Between Valuation and Accounting As a business enters the fundraising zone, every number is now in play. Investors are not only looking at

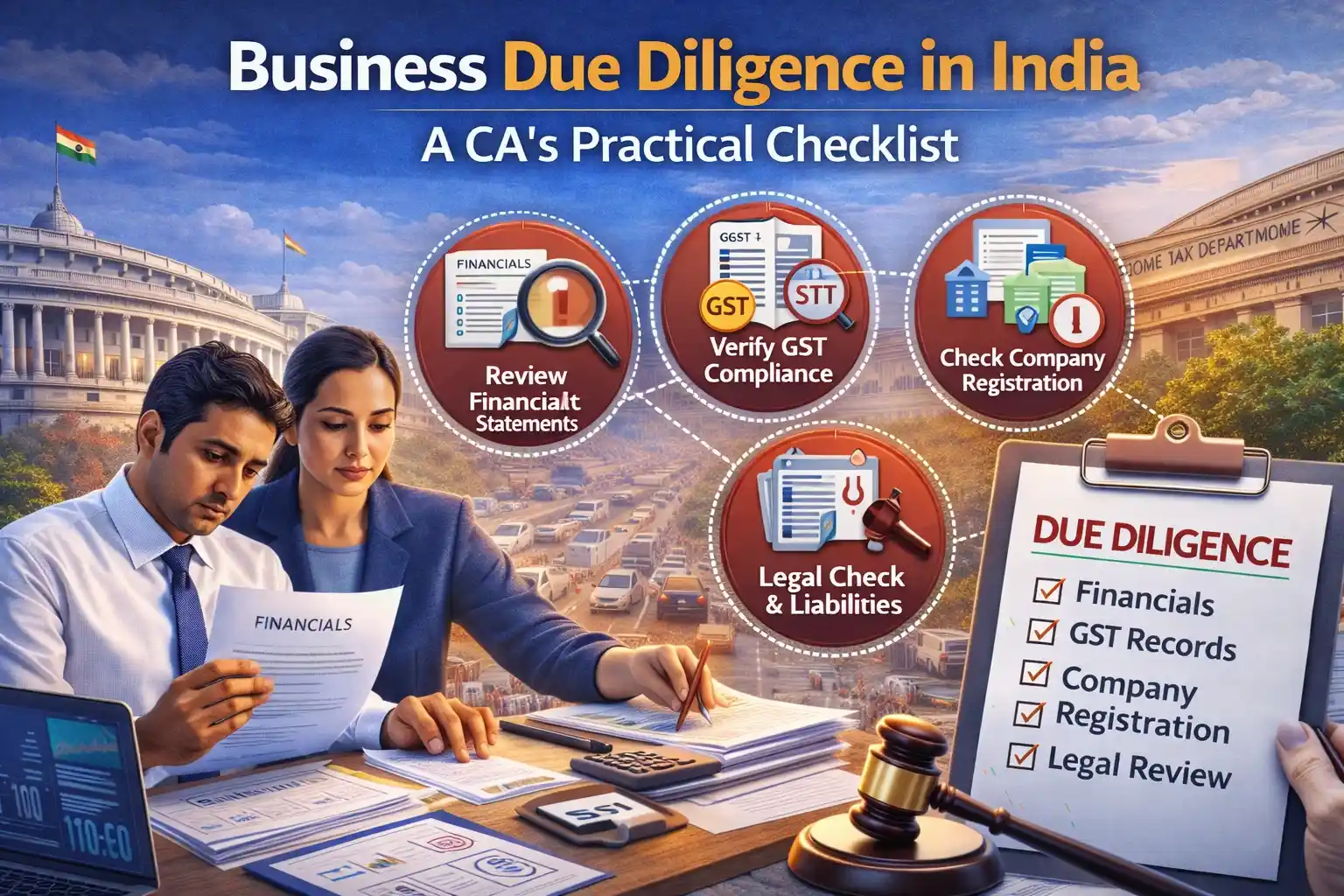

The Importance of Due Diligence in an Acquisition(Transaction) for Start-ups. Purchasing an existing business in India can be a valuable shortcut to expansion. It provides access to