Introduction

FDs or Fixed Deposits are amongst the most popular investment avenues in India due to their safety and predictable returns. But many investors forget the key question — tax on the interest income. It is essential to understand how income tax on fixed deposit is levied to plan your finances in a better manner and avoid any unwarranted tax liabilities.

Learn More About Fixed Deposit Interest Income

Interest on Fixed Deposit is the interest income received from an amount, which the depositor deposits with a bank or financial institution for a fixed duration. The interest that is applicable might be was, normally either monthly, one-fourth of yearly or at a maturity point.

Even if the interest is reinvested and not taken out, it will be treated a taxable income that year.

Taxability of FD Interest Income

Interest from Fixed Deposits is fully taxed at the maximum level under the head of income as Interest income – “Income from Other Sources.” This is added to your total income and taxed at an applicable income tax slab.

Please Note: FD interest does not offer tax-free profits like certain other investment options. Thus, you should calculate and report your earnings accurately.

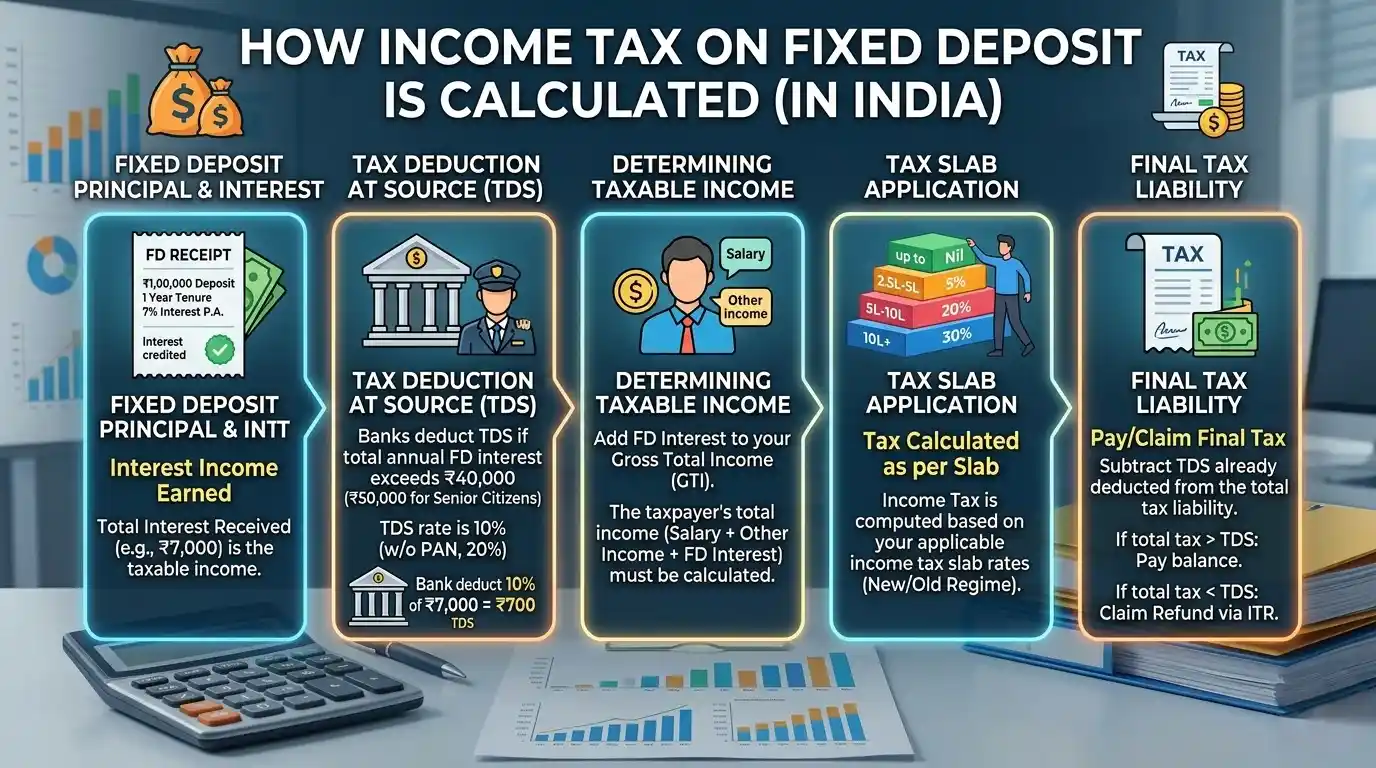

How to Calculate Tax Paid on FD Interest {Step By Step}

Step 1 — Total Interest Earned ⋙⋈

⋈◔❆

⋈◔❆

The first thing is to calculate the aggregate interest earned on all Fixed Deposits in a financial year. You can find this information in the bank statement or interest certificate.Step 2: Total-income + Interest

Then include FD interest from the last year in your income (salary, business income, etc.) to reach out.Step 3: Determine Tax Slab

Tier slabs applicable to you depend on your total income. Tax on FD interest will be as slapped by your slab rate

Step 4: Calculate Total Tax Due

Compute the overall tax payable on your total income (including FD interest) by multiplying with your tax rate.Understanding TDS on Fixed Deposits

Banks levy TDS on the Fixed Deposit (FD) interest exceeding a certain limit. Right now, TDS is deducted on interest income above ₹40,000 in a financial year, and ₹50,000 for senior citizens.If PAN is given, then standard TDS rate will be 10%. Without PAN, the rate may increase much higher than that.TDS vs Actual Tax Liability

TDS is not the final tax. It was just some advance taxation taken out.If your final marginal tax rates beyond the one at which you paid TDS, rest when you file your Income Tax Return (ITR) return needs to be paid. On the other side, if TDS has been deducted in excess, you can apply for refund.Significance of Form 26AS & AIS

It provides the details of interest income and TDS deducted with the respect to Form 26AS and annual information statement (AIS).The documents aid in verifying the income details, ensuring that all your earnings are reported correctly in your ITR.Advance Tax on FD Interest

Advance tax is to be paid if your total tax liability during a financial year is more than ₹ 10,000.Interest earnings on FD will be included in the calculations for advance tax. Non-compliance in this regard, invites default interest under Sections 234B and 234C.Old vs New Tax Regime

So, FD interest income is fully taxable under both old and new tax regimes. That said, the actual tax liability can fluctuate based on deductions and slab rates.Taxpayers will have to compare the two and pick whichever regime provides greater savings.Common Mistakes to Avoid

Most taxpayers think that if TDS is deducted, then nothing has to be done. This is not true, the tax calculated at year end can be different. Likewise, we often see a mistake where FD interest is not reported unless actually received in cash. Interest is subject to taxation on an accrual basis, irrespective of a withdrawal.

Role of Professional Guidance

Tax calculations relevant to Financial year can be complicated as we might have multiple fixed deposits or income sources.GSCCA is a Delhi based firm rendering advisory and consultancy services in the field of GST and company registration which helps Individuals/business to handle tax filings seamlessly. Note: In order to ensure detailed reporting of Income tax & returns online, and compliance with tax laws in a much more systematic manner, making use professional help is highly advised yet providing its content informative.

Tips for Better Tax Planning

Asset allocation can help limit taxes on growth. Interest income falls into this category, and if you track it all year, you can plan for its taxation rather than be surprised at the last minute.Well kept records and timely review of financial statements allows for accurate filing.

Benefits of Proper Tax Calculation

Correct tax computation prevent penalties, notices, and legal troubles. Also makes ITR filing easier and quicker refunds (if applicable).Well handled compliance hones financial discipline as well as credibility.

Conclusion

Every investor needs to know how income tax on fixed deposit is calculated. As FD interest is taxable in full, it needs to be included as part of the total income and taxed at the applicable slab rates. Through good record-keeping, accurate reporting of income and effective planning, taxpayers can invest in FD to get their interest income taxed efficiently and remain tax compliant.